On June 1, the Forex Blog reported that Brazil is considering a forex tax on capital inflows as a way of discourage the inflow of speculative capital that is causing the Real to appreciate. It turns out that Brazil is not alone; England and France, among others, are also mulling taxes on forex transactions. Their goal is not necessarily to discourage capital inflows, but rather to raise money to fund projects that would otherwise not be viable under current budgetary conditions. The UK “levy would raise $30bn-$50bn a year - enough to double spending on health in low-income countries.” The French plan, meanwhile, would “involve taking 0.005% of the proceeds of currency transactions, perhaps on a voluntary basis, to benefit global aid projects.”

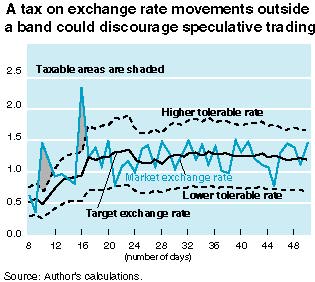

While Brazil and England/France appear to be pursuing different ends, together their plans capture the idea behind the “Tobin Tax.” Originally proposed by Nobel Laureate James Tobin after President Nixon declared the end of the gold standard, the tax would be levied on all forex transactions with the proceeds deposited in forex stability funds. One of the most popular versions would only impose the tax during periods of volatility (i.e. speculation) so as not to punish those exchanging currency for “mundane” reasons.

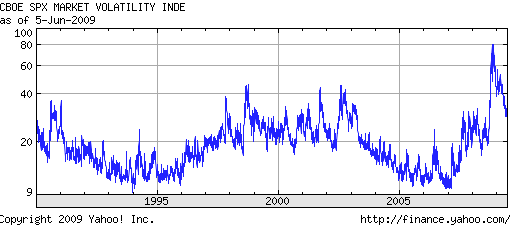

While still a fringe idea, the tax initially gained momentum following the 1997 Southeast Asian economic crisis, and has found new followers in the wake of the ongoing credit crisis. Consider the unprecedented volatility in currency markets of late, manifested in wild daily fluctuations.

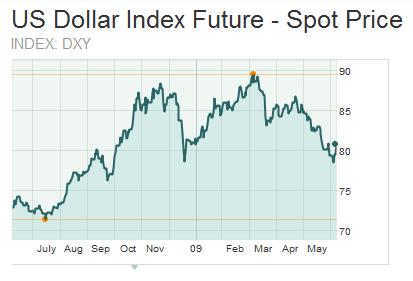

Even the US Dollar, the world’s reserve currency, has been on a veritable roller coaster of late, rising and falling by 10% in a matter of months. Prior to the rise of forex speculation (already a $1 Quadrillion/year market!), it was rare for a currency to move that much in a year. Given that such speculation probably accounts for 90% of daily turnover, it seems obvious as to who is causing this volatility.

Don’t get me wrong; there’s a role for speculation in the forex markets, just like there’s a role for speculation in all securities markets. When markets function efficiently and players act rationally, currences should and will reflect economic fundamentals and act to minimize global imbalances. Due to the rise of the carry trade and the herd mentality, however, the oppose often obtains in practice. This can cause currency runs and or artificially inflated currencies that compel Central Banks to act counter to the way they otherwise would (i.e. by raising interest rates rapidly to deter capital flight, crimping economic growth.)

A Tobin tax would work both to minimize speculation in the short-term (by taxing trades) and promote stability in the long-term (by providing Central Banks with funds that they can use to fight speculative “attacks.” Besides, given that forex traders already enjoy favorable tax treatment - i.e. taxed below the short-term speculative rate - it wouldn’t be the end of forex trading as we know it.

Source:www.forexblog.org